Life insurance carriers face a short-term future in which costs can be substantially reduced and the nature of work as well as the tasks team members take on will be drastically altered. New opportunities to create custom products and more targeted marketing and sales will be exposed. And customer experience will become more and more frictionless.

All thanks to AI.

…If we get it right.

Getting it “right” is a task larger than just building a nice AI solution. “Right” involves many considerations around data and digital architectures that when delivered with equal consideration and effort, enables the promise of AI to be fully realized. With that important caveat in mind let’s look at the current landscape of insurer AI implementations, challenges that have been uncovered and 12-24 months priorities for carriers around the globe to see how we’re doing.

What’s going on? The current state of readiness for AI in life insurance

In order to assess the current state of an organization’s AI readiness, data readiness is an equally important consideration. Equisoft and UCT partnered with LIMRA to conduct a global research study focusing on key areas of AI implementations and the prioritization of AI projects along with an assessment of data readiness

That study revealed some interesting findings about what insurers are doing right now, what challenges they are facing and what they plan to do next.

The results were surprising...

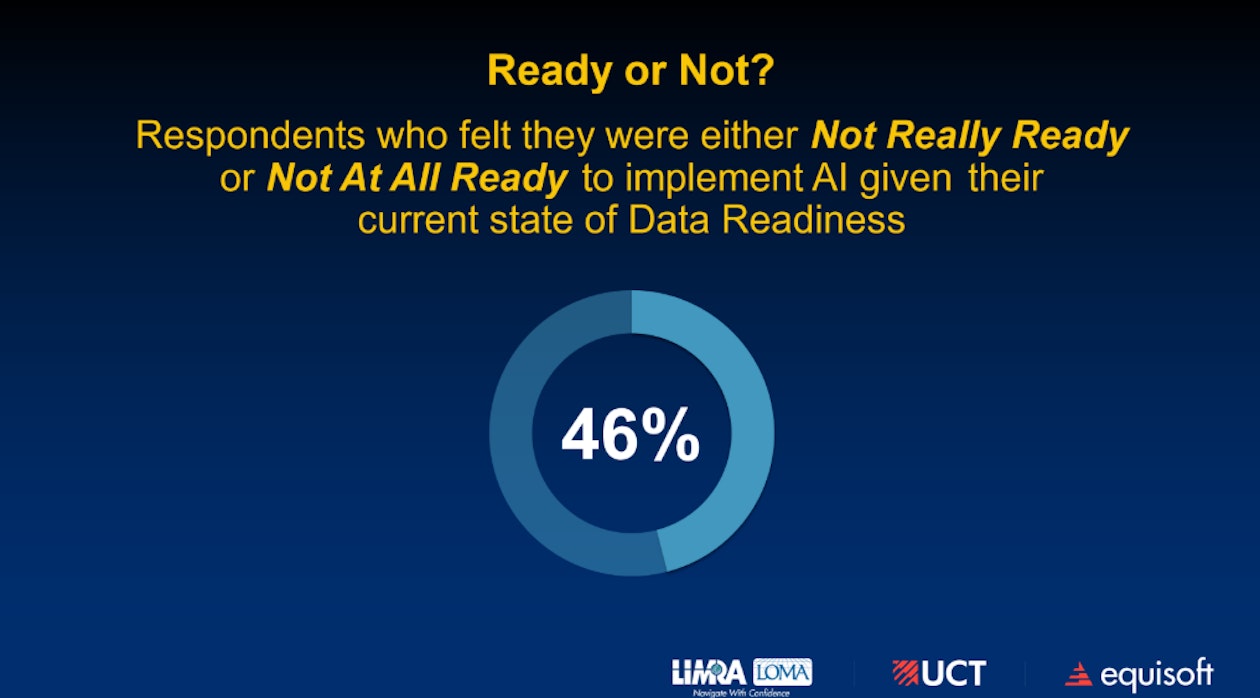

Although companies in every region around the globe reported that their data readiness is at the progressive (or second highest) maturity level, 46% of respondents say they just aren’t ready to tackle AI yet.

Why?

Most—a whopping 78%--cite their data as the biggest stumbling block.

In some cases, the apparent disconnect comes from the fact that companies have done a good job of putting data foundations in place—for most current data use cases. They are able to make data available, with good accuracy, in real time for digital sales and service solutions. But that doesn’t mean their data is ready for the primetime demands AI will make.

In other words, their data is in good shape for the needs of the present. But not quite ready to meet the demands of tomorrow’s more advanced tech.

In order to fully prepare, companies must now take the next steps in optimizing data across the dimensions of:

- Data governance

- Sourcing and integration

- Analytics

- Data Quality and Integrity

- Infrastructure

- Organizational Alignment

Current AI Adoption in Life Insurance

The research indicates that the highest current use of AI is in Operations, closely followed by New Business. Other areas with significant AI adoption rates include Customer Service, Underwriting, and IT.

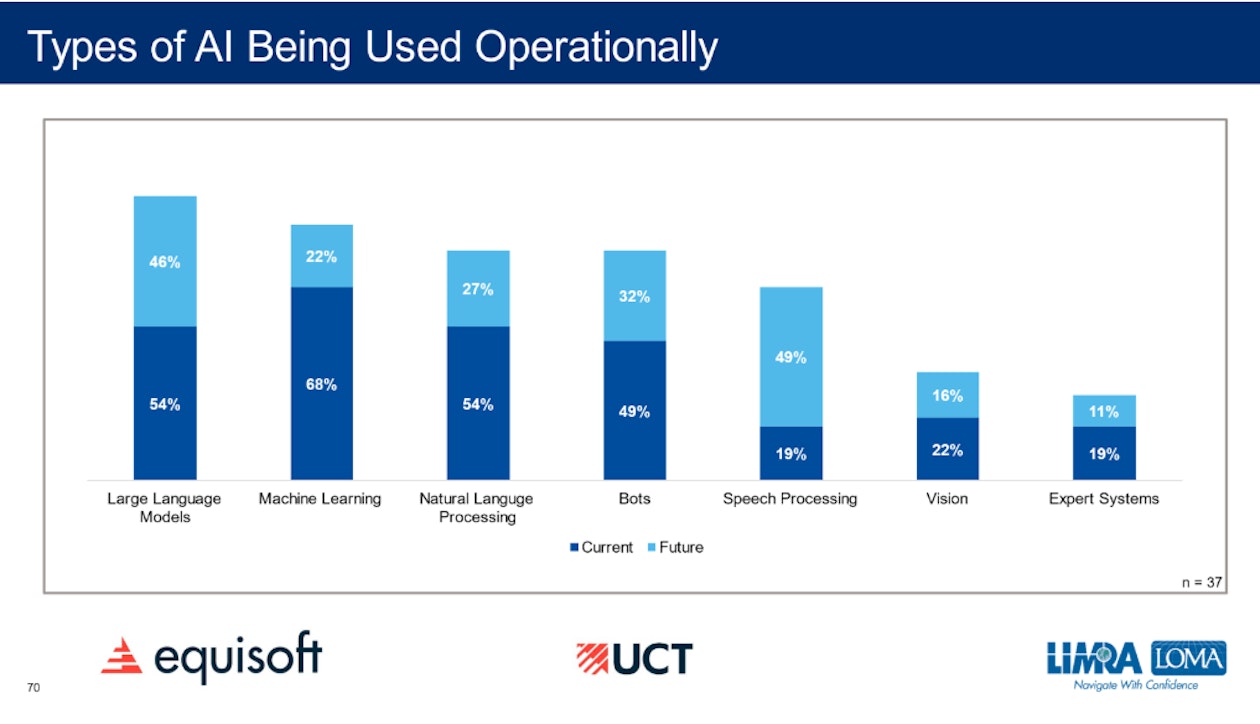

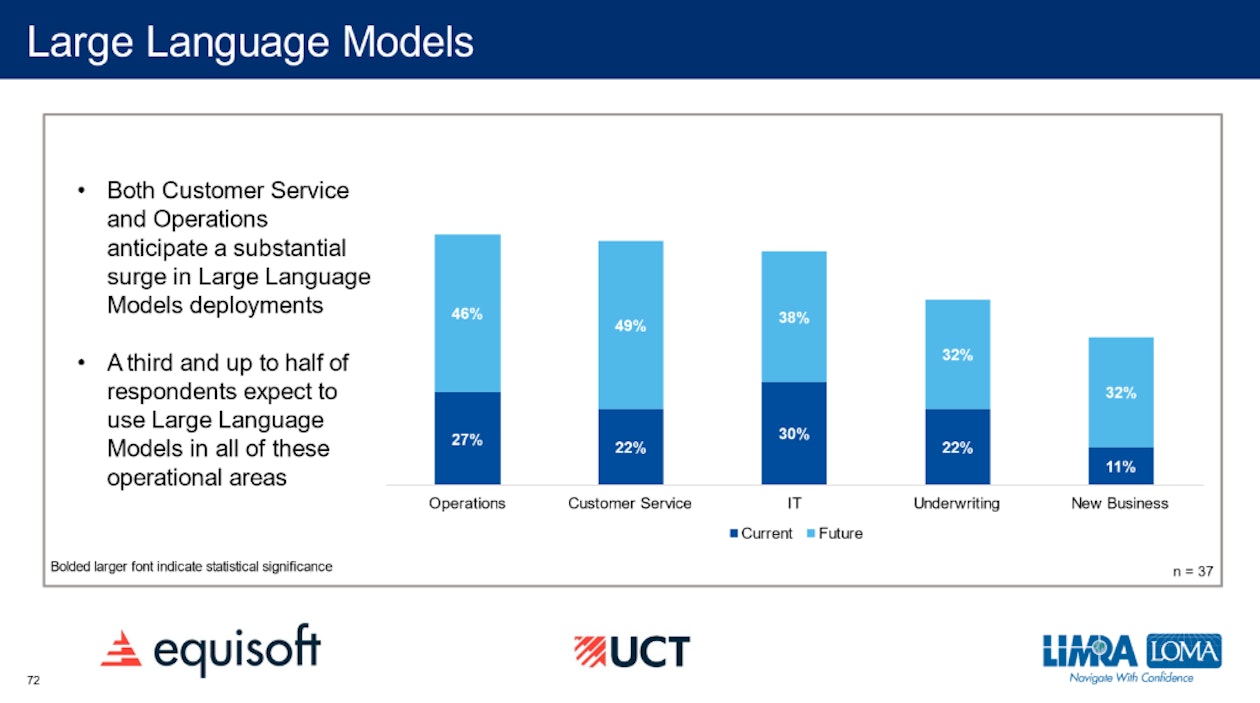

Although various types of AI are already utilized within life insurance companies, a primary focus currently is on Large Language Models (LLMs). Over half of the surveyed companies are already implementing LLMs across their organizations, and within two years, all surveyed companies expect to have LLMs operational within their businesses.

Customer Service (48%) and Operations (46%) are identified as the areas where LLM adoption is anticipated to provide the greatest value. Currently, LLM usage is most prevalent in IT departments but is expected to expand throughout companies, impacting Operations, Customer Experience (CX), Underwriting, and New Business.

Bots are currently used by about a quarter of the respondents in customer service applicants. It’s expected that adoption will reach 75% in the next two years.

Machine Learning is used by 40-50% of respondents for Operations and Underwriting for things like:

AI Use Cases in Life Insurance Administration

There are many use cases for LLMs in Customer Service, Operations, Underwriting, New Business and IT in life insurance organizations? Some of the ways that insurers are currently testing AI include:

Customer Service Use Cases #

- Automated Query Resolution: LLMs can handle routine customer inquiries about policy details, coverage, premium payments, and basic claims status, providing instant responses while escalating complex cases to human agents.

- Predicting customer churn

- Routing inquiries to appropriate teams based on complexity

- Forecasting call volumes

- Policy Document Analysis: LLMs can quickly scan through policy documents to answer specific customer questions about coverage terms, exclusions, and benefits, making customer interactions more efficient.

- Multilingual Support: Providing 24/7 customer support in multiple languages, enabling insurers to serve diverse customer bases more effectively.

Operations Use Cases #

- Document Processing & Data Entry: Using Ai enabled OCR to automate the extraction and classification of information from various documents like medical records, application forms, and claims documentation.

- Form classification to automatically route documents

- Data validation to catch errors and inconsistencies in submissions

- Automated data completion by inferring missing fields

- Quality Assurance: Reviewing customer interactions, documentation, and processes for compliance and quality standards, flagging potential issues for human review.

- Process Optimization: Analyzing operational data to identify bottlenecks or resource constraints and suggesting process improvements based on patterns and inefficiencies detected.

- Identifying optimal workflow routing

- Forecasting processing volumes and staffing needs

- Detecting process deviations and inefficiencies

- Claims Processing: Fraud detection using anomaly detection algorithms to identify suspicious patterns

- Automated classification of claims documents and correspondence

- Predicting claims processing time and resource requirements

- Identifying claims likely to become complex or require escalation

Underwriting Use Cases #

- Risk Assessment Automation: Analyzing medical records, lab results, and application data to provide initial mortality risk assessments and recommendations for underwriters.

- Medical impairment analysis using structured and unstructured health data

- Lab results interpretation and trending

- Medical records summarization

- Identification of relevant medical history

- Correlation analysis between conditions

- Lifestyle risk assessment using available behavioral data

- Credit risk scoring for premium payment default risk

- Data Enrichment: Combining information from multiple sources to create comprehensive risk profiles and identify potential red flags.

- Decision Support: Providing underwriters with relevant similar cases and precedents to help inform their decisions while maintaining consistency in risk assessment.

- Price Optimization: Dynamic pricing based on risk factors.

- Price elasticity modeling

- Competitive pricing analysis

- Customer lifetime value prediction

New Business Use Cases #

- Application Processing: Streamlining the application intake process by automatically extracting and validating information from submitted documents.

- Requirements Management: Identifying missing documentation or information needed to complete applications, automatically generating requests for additional information.

- Automated triage of applications by complexity.

- Risk class prediction to streamline underwriting

- Early identification of likely declines

- Market Analysis: Analyzing market trends, competitor offerings, and customer feedback to inform product development and pricing strategies.

IT Use Cases #

- Code Documentation: Automatically generating and maintaining documentation for legacy systems and new development projects.

- System Integration: Helping create and maintain APIs and integration points between different insurance systems and platforms.

- Incident Management: Analyzing system logs and error reports to identify root causes of issues and suggest potential solutions.

- Test Automation: Generating test cases and scenarios based on system specifications and user stories.

Cross-Functional Applications #

- Knowledge Management: Creating and maintaining centralized knowledge bases that can be accessed across departments. Useful for summarizing long or complicated articles and providing easily digestible key messaging.

- Training and Development: Generating training materials and providing interactive learning experiences for staff across different departments.

- Compliance Monitoring: Scanning communications and processes across departments to ensure adherence to regulatory requirements and internal policies.

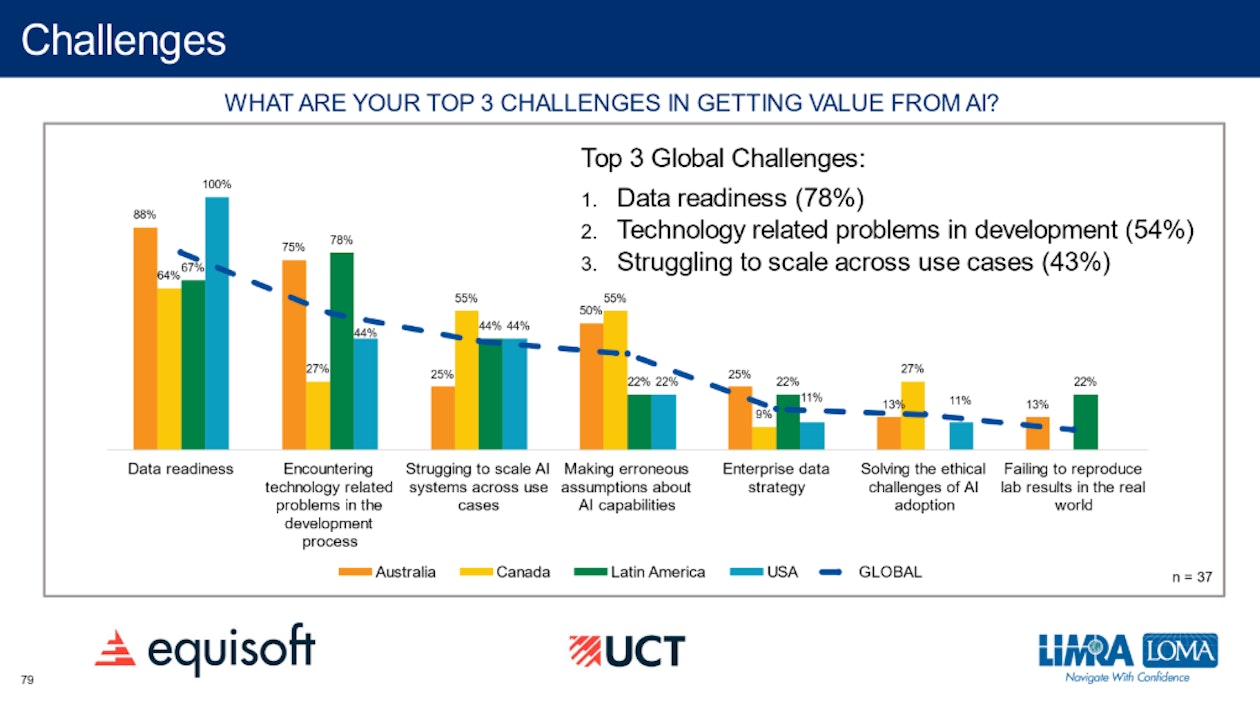

The Top 4 Challenges in Getting Value from AI

Data readiness #

One of the largest challenges faced by organizations looking to implement AI initiatives is ensuring data readiness. Preparing data for use in AI applications requires that the data is first exposed and available, which can be a challenge when the data is stored in legacy systems. Data readiness also involves having clean, accurate, and well-organized data that can be effectively used by AI systems. Without proper data management, AI initiatives are likely to falter, leading to suboptimal outcomes.

Unexpected technology issues #

Many Insurers often encounter technology-related problems during the development process. These issues can range from inadequate infrastructure to compatibility problems between new AI tools and existing systems. Overcoming these barriers requires significant investment in technology upgrades and skilled personnel.

Struggling to scale AI systems across use cases

While developing a successful AI model for a specific task is challenging, expanding its application to different areas within the organization often presents even more complexities. Achieving scalability requires robust frameworks and strategies for deployment and maintenance.

Making erroneous assumptions about AI capabilities

Some organizations discovered they had an overly optimistic view of what AI can achieve, leading to unrealistic expectations and potential project failures. It is crucial to have a clear understanding of AI's limitations and to set realistic goals.

Lower ranking challenges in implementing AI

Enterprise data strategy

#

Although some challenges rank lower, they shouldn’t be considered negligible, as is the case when insurers run into difficulty because they haven’t developed an effective enterprise data strategy. This is a fundamental success factor for AI implementation and involves creating policies and practices for data collection, storage, and usage that align with the organization's business objectives. Without a well-thought-out data strategy, AI projects may struggle to deliver value.

Solving the ethical challenges of AI adoption

Solving the ethical challenges of AI adoption is not negotiable. This includes addressing concerns related to bias, transparency, and the potential impact of AI on jobs. Ensuring ethical AI practices is essential for gaining stakeholder trust and avoiding negative repercussions. These are complex issues that take a lot of time, effort and judgement to process. Things are made even more difficult in many cases because AI implementations are not always transparent about how they arrived at an output, so it can be challenging to root out legacy bias or incorrect information.

Failing to reproduce lab results in the real world #

AI models that perform well in controlled environments often face unexpected challenges when deployed in dynamic, real-world scenarios. Bridging this gap requires rigorous testing and validation procedures to ensure the reliability and robustness of AI solutions.

Life Insurer AI Priorities for the Next 12-24 Months

As the above results show, LLM customer service use cases are the biggest planned investments for carriers. But adoption of AI in all the above areas is expected to happen across the next 2 years for more than 80% of respondents around the world.

This is a fast-moving train and companies will need to act quickly in order to keep up with competitors who start to gain CX, efficiency and decision-making advantages.

When asked to comment on why their company is either considering future AI implementations or not CIOs made the following observations which reveal the fragmented nature of insurers’ readiness for AI.

We intend to implement AI use cases over the next 2 years

- “There are plenty of opportunities for AI that will improve job satisfaction, quality, and productivity without having any impact on a consumer.”

- “Enable iterative learning; prove out Gen AI opportunities.”

- “Allows the organization to focus initial deployments to high value / low risk use cases to test value and adoption.”

We are not yet ready to implement AI solutions

- “We are in a process of data normalization and process optimization.”

- “Still implementing foundational elements…”

- “No focus at this time.”

- “Not currently prioritized.”

The Near-Term Future for AI in Life Insurance

When asked, “How AI will transform your organization and benefit stakeholders in three years?” CIO responses included:

- “Ultimately, we view AI as being a pervasive technology that will be deeply ingrained in all aspects of the operation wherever technology is employed. Generative AI will be no different than the internet's disruption to computing in the enterprise.”

- “AI will be used by employees across the organization for everyday tasks, making them significantly more productive. It will be used to improve the customer experience while never being allowed to negatively impact a customer.”

- “In 3 years, we may have some level of an enterprise-wide success for AI, but I suspect…that we will see pockets of successful implementations on small scales - either at the departmental or individual level. Success will be more bottom up than top down. While AI may represent a potential exponential shift in many areas over time, the limiting factor for us will be organizational, driven largely by ROI considerations. We have a long way to go in terms of technical mastery (both in IT and in the business), governance (including data governance), cost, and organizational commitment...I see years 3-6 as being more impactful.”

Wrap Up #

While the implementation of AI solutions in life insurance is still in its infancy, the potential for transformation is immense. Current efforts are focused on data normalization and process optimization, laying down the foundational elements necessary for future AI integration. Although AI is not currently prioritized, the outlook for the near term suggests a gradual but impactful adoption.

Looking ahead, AI is expected to become a pervasive technology, deeply ingrained in various aspects of operations. It will enhance productivity, improve customer experiences, and drive organizational efficiency. Despite the challenges of technical mastery, governance, and cost, the next three to six years could see significant advancements at departmental and individual levels, driven by a bottom-up approach.

For life insurers aiming to successfully implement AI, the key lies in developing a robust data governance framework, investing in technical expertise, and fostering an organizational commitment to innovation. By addressing these areas, insurers can pave the way for AI to become a cornerstone of their operations, delivering substantial benefits to both the organization and its stakeholders.